Foreclosure 101 for First Time Homebuyers

Foreclosure 101 for First Time Homebuyers

By Julie Marion, Founder of The First Time Homebuyer Workshop

What Is Foreclosure?

Foreclosure (either judicial or non-judicial) is the process the bank or lender takes to legally take title to your property should you default on your mortgage (On the street the process is also called keys for deed).

Are you worried what happens if you miss a mortgage payment, two or three? Learn the foreclosure timeline by state, your rights, and better alternatives to avoid financial disaster.

Everything is all hunky dory when buying a house, until it's not. Understanding what happens if you miss payments, what the process is and how to avoid foreclosure all together is prudent.

Quick‑Glance Takeaways

- Foreclosure can happen to anyone - even buyers with solid jobs and down payments.

- Each state follows a judicial or non‑judicial process (some allow both).

- You can stop foreclosure up to the day of the auction if you act fast.

- Alternatives like loan modification, forbearance, and short sales often hurt your credit far less than foreclosure itself.

The smartest move: build an emergency fund before you house‑hunt and stick to your budget. All the salespeople leave after the transaction is over and so you need to know exactly what's in store before you sign the purchase contract.

Best Advice: Know your numbers!

Why First‑Time Buyers Need A Foreclosure Game Plan

More than half of first‑time homeowners report some level of buyer’s remorse. In late 2023, total home‑buyer remorse spiked to 92 percent across all buyer types. One of the biggest regrets? Paying too much and not understanding the consequences of missed mortgage payments.

Knowing the foreclosure rules in your state—and the lifelines you can pull if money gets tight—lets you shop confidently, negotiate smarter, and sleep better in your new home.

Foreclosure Basics: Definitions & Key Steps

Foreclosure is the legal process that allows a lender to seize and sell your new home when the borrower stops making mortgage payments. The timeline generally follows six milestones:

- Payment Default – You miss the due date (usually the 1st) and the 15‑day grace period.

- Notice of Default / Demand Letter – Arrives after roughly 30–45 days past due.

- Formal Foreclosure Start – At 120 days late, the lender can file a lawsuit (judicial) or record a notice of sale (non‑judicial).

- Pre‑Sale Period Varies by state; you can still reinstate the loan.

- Foreclosure Sale / Auction – Property goes to the highest bidder or reverts to the bank as something called "REO property" (Real Estate Owned property).

- Eviction – Borrower must vacate (often within three days) or face a court‑ordered eviction.

Good news: You can halt the process at any stage by curing the default, negotiating a workout, or selling the property.

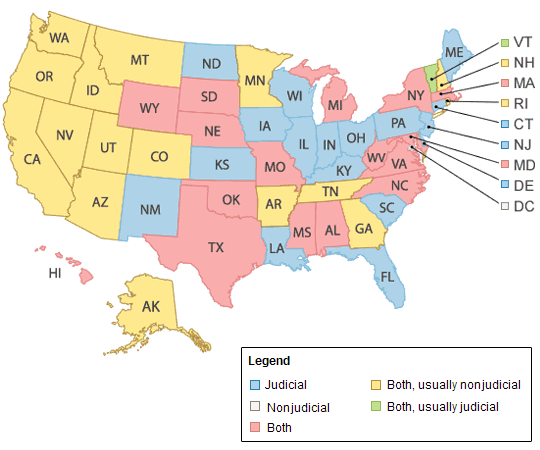

Judicial vs. Non‑Judicial Foreclosure Processes By State

Map Graphic Courtesy of Bank Rate

Timeline Of Foreclosures

Judicial states require the lender to sue in court, often stretching the timeline years (Hawaii averaged 2,070 days in 2021). Non‑judicial states can foreclose in months (Montana averaged 94 days in 2021).

State Averages ~ How Long Foreclosure Takes

|

State Average Days |

State Fastest Days |

|

Hawaii - 2,070 days |

Montana – 94 days |

|

Nevada 1989 days |

Wyoming 102 days |

|

Kansas 1901 days |

Mississippi 133 days |

|

New York – 1,659 days |

|

Statistics from Q3 – 2021

If you want to verify or look at more information about foreclosure a trusted site is ATTOM. They report on foreclosures and what’s happening in the market.

Top Triggers That Push First‑Time Buyers Into Default

- Sudden job loss or reduced hours

- Major medical bills or disability

- Divorce

- Loss of income when starting a family – Day care expenses, or one spouse staying home

- Natural disasters and uninsured property damage

- Sharp interest‑rate increases on adjustable mortgages – or a combination of interest rates, property tax and energy cost increases

- Rising property taxes, HOA dues or increases in Homeowner insurance

Foreclosure Alternatives That Save Credit & Equity

|

Option |

When to Consider |

Key Points |

|

Loan Modification |

Income dropped but still steady |

Lender may lower rate, extend term, or switch to fixed‑rate. |

|

Forbearance |

Temporary hardship (illness, layoff) |

Payments paused or reduced; balance repaid later. |

|

Refinance |

Equity & credit still strong |

Replaces the current loan with one you can afford. |

|

Short Sale |

Owe more than home value |

Lender agrees to a below‑balance sale; credit hit is lighter than foreclosure |

|

Deed‑in‑Lieu |

No buyer for short sale |

Voluntary hand‑over of title; may receive “cash for keys.” |

Tip: Always start with the lender’s loss‑mitigation department, not the general customer‑service line.

Questions Answered On What To Do If Foreclosure Is Near

What happens if you miss a mortgage payment?

- Call your mortgage servicer before the 30‑day mark.

- There will be a lot of fees in addition to the regular payment.

- Document the hardship (pay stubs, medical bills, termination letter).

- Ask about modification, forbearance, or reinstatement options.

- If you’re buried, consult a HUD‑approved housing counselor (free) or real‑estate attorney.

- Consider a second job/income.

How to avoid foreclosure for a first-time homebuyer, some final thoughts for future homeowners

- A healthy emergency fund (ideally 3–6 months of expenses) is the best foreclosure insurance.

- Learn each step of the mortgage, appraisal, inspection, legal, and real‑estate professions before you shop.

- Stay proactive foreclosure isn’t inevitable unless you ignore the warning signs.

Like what you are learning here? You don’t have to navigate the homebuying process alone. Choose the path that’s right for you — whether that’s the free mini-class or the full workshop — and let’s get started today!

🎁 Free Mini‑Class ▶ "Homebuying Chaos Unwrapped"

Ready to get all five professions demystified in one sitting? Join our no‑cost class before you start house‑hunting!

🚀 Go Deeper with the First‑Time Homebuyer Workshop

Join the Full Workshop ▶ "The First Time Homebuyer Workshop"

The full workshop bundles detailed checklists, worksheets, and weekly Q&A sessions with me and industry experts—so buyer’s remorse never stands a chance.

Let’s demolish homebuyer remorse together—one empowered buyer at a time.

Julie Marion

Founder of The First Time Homebuyer Workshop, homebuyer educator, Urban Planner, Freddie Mac Credit Counselor, Real Estate Broker, Podcast Host, You Tube Contributor.

Looking to learn a little more? Check out our FREE Class where you learn how the industry is organized!